Yield to worst

"The food is terrible," to quote the famously ambivalent restaurant review--"and the portions are so small." Much the same can be said of today's junk-bond market. The yields are terrible--and there's not enough new supply to satisfy the clamoring demand.

The subject at hand is the worldwide yield famine; the special point of focus is how to turn that distress to profit. You know that income-seeking Americans are scraping the bottom of the barrel. It's the same on the other side of the Atlantic. According to Friday's Financial Times, income-deprived Continental investors are bidding up speculative-grade debt from the European "periphery" to prices higher than comparably rated securities emanating from the European "core." Yield is the thing, even if you'll never get it. All in all, we conclude, the junk market--we are now back in North America--is ripe for the risky art of short selling.

Even in what the adepts call a "crowded" trade, the short seller's way is lonely. You, the man or woman inside the bear suit, conceive a point of view that usually does not comport with authorized institutional thinking. Let us say that you believe that stunted yields, receding credit quality and rising interest rates (or the threat thereof) have delivered an opportunity to sell short junk bonds or the mutual funds and exchange-traded funds that house them.

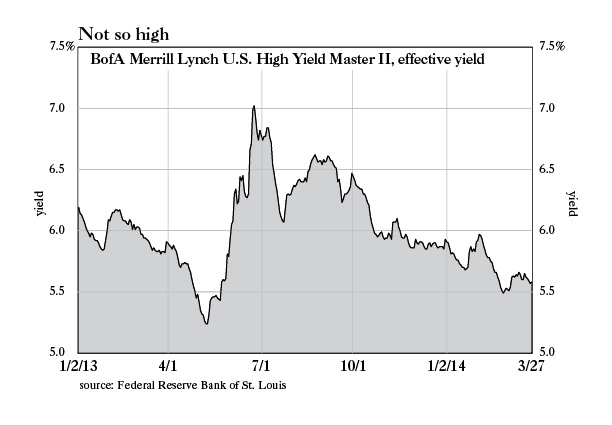

BofA Merrill Lynch U.S. High Yield Master II, effective yield

You take a walk around the block to interrogate yourself: Do you really want to do this thing? Normal people buy first and sell later. Short sellers reverse the order by selling borrowed securities first with the intention of buying later to close out the transaction (or, in the idealized short sale, never having to cover because the securities they shrewdly sold have become worthless). It's not always easy to get "the borrow." Nor is it usually expedient to remit to the securities lender the dividend or interest payment on one's borrowed stock or bonds. You, contemplating the advisability of becoming a short seller, take the measure of the known risks--rising markets, Federal Reserve "stimulus," peace and prosperity, etc. You add, as well, the high personal costs that short selling sometimes exacts--insomnia, heartburn, hair loss, paranoia. And having duly considered the pros and cons, you gamely exclaim, "Heck, yes!"

We write not mainly for these blithe, intrepid spirits--how many can there possibly be?--but for all who lend or borrow. As leverage is ubiquitous, so is credit topical. Besides, today's junk-bond market is a living laboratory in the consequences of radically easy monetary policy.

At the highs of junk-bond prices last May 9--this was on the eve of the 2013 tapering fright--the Bank of America Merrill Lynch U.S. High Yield Master II Index fetched 5.24%. The subsequent scare over the possible end of QE quickly pushed the average yield to 7.02%--178 basis points in only 33 trading days. Having sold the tapering rumor, the junk market proceeded to buy the news. So here we are at 5.63% on the same BofA Merrill Lynch index, a quarter point above the old lows in yield.

The contention here is that today's market is bereft of absolute value and low on the relative kind. The 2007 market was, we think, zanier on account of the higher incidence of leveraged buyout debt, but today's market is diligently closing the gap. "It's getting junkier," says Michael E. Lewitt, CIO of Eccles Street Asset Management LLC and editor of The Credit Strategist. "The ratings are slipping more. In terms of 'covenant lite,' [loans or bonds issued with a minimum of restrictions intended to enforce financial discipline on the borrower] a couple of years ago when covenant lite really started picking up, it really was just the strongest borrowers that the market would grant that kind of package to. That's no longer the case. Anybody can get a covenant lite package. The market is much less discriminating. The complacency has set in. Covenants are weakening in the loan market.

"In the bond market," Lewitt continues, "covenant packages are weaker and there has been some erosion in call protection. Historically, there has been five-year, non-call protection on bonds; we're seeing episodes of three years. In general, most deals that are coming to the market are not for newly minted LBOs. The bad news is they are often to pay dividends to equity sponsors to re-lever companies and that is never a good thing."

At current ground-scraping interest rates, "high" yield is an oxymoron. Many regret this state of affairs, though not the bears. A 15% coupon makes for a prohibitively expensive short sale (remember, the bearish speculator must pay the securities lender the interest he or she would have otherwise received through ordinary corporate channels). A 5% coupon alone won't make for a profitable short sale, but it gives the bears a fighting chance.

We serve up four vignettes in support of this thesis. No. 1 concerns a transaction that captures the market's manic mood. No. 2 is about a liquid, overpriced, vulnerable bond that seems ripe for a short sale. No. 3 is a case study in what a Chartered Financial Analyst might call heavy competition overlaid on lousy fundamentals. No. 4 is an update on Intelsat, an over-leveraged borrower with an underachieving income statement.

The first evidentiary item concerns a February financing by BlueLine Rental for the purpose of enabling the promoters of a private-equity deal to take out 100% of their equity not two weeks after they'd put it in. According to Matthew Fuller of the LCD unit of Standard & Poor's, not since 2007--that fateful year--has any dividend recap deal followed so quickly on the heels of the closing of the acquisition as has BlueLine's.

BlueLine Rental, successor to the Volvo equipment rental business, rents backhoe loaders, skip loaders, track dozers, trenchers, skid steers, wheel loaders, boom trucks, knuckle lifts, electric man lifts, towable booms, welders, light towers, pumps, heaters and other capital items suitable for an expanding economy. The company does business at 132 rental locations; it serves 45,000 customers in 44 states, Puerto Rico and a pair of Canadian provinces.

BlueLine is a "rollup," the product of the consolidation of scores of equipment-rental franchisees into a centrally owned retail network. Platinum Equity, a Beverly Hills-based private equity shop, did the rolling. The price tag was $1.1 billion.

A senior bank line and $760 million of single-B-rated, 7% second-lien notes of February 2019, offered at par, financed the acquisition. That is, those borrowings financed the first phase of the acquisition. Demand for the 7s being unslaked, investors asked for another opportunity to participate in the leveraging up of a cyclical, macroeconomically sensitive business. BlueLine obliged with $252.5 million of triple-C-rated 93/4s of 2019 at 99.

Isle of Capri Casinos’ stock price

Here was a double homage to booms gone by. Beyond the use of proceeds (a dividend for Platinum Equity) was the fact that the 93/4s are payment-in-kind, or PIK, notes; "toggle," too, is a part of the description. In certain circumstances, the borrower may choose to pay interest not in cash but in additional securities (in so choosing, it is said to toggle between one form of payment and another). Like the crocus or snowdrop, PIK securities are seasonal heralds of warmth and optimism. Their appearance in the capital markets is a sign that cyclical winter is past and that a new season of lending and borrowing is bursting forth.

The 93/4 notes pushed leverage for the borrowing entity to 5.9 times the favored, if not officially sanctioned, measure of cash flow called "pro forma, adjusted EBITDA." That was up from 4.6 times before the new PIK issue came into the world. (EBITDA, you know about: net income before net interest expense, taxes, depreciation and amortization; the "adjustments" applied to EBITDA include those related to other non-cash charges, brand license royalties and "estimated costs we expect to incur operating as a stand-alone entity," instead of, as before, a collection of franchised businesses.) This 5.9 times leverage compares to 3.2 times net leverage at double-B-rated United Rentals Inc. (URI on the NYSE), BlueLine's larger and publicly traded competitor, and to just under four times debt-to-EBITDA for the entire high-yield bond universe, according to a March 28 report by Morgan Stanley.

No mystery what's in this transaction for the private-equity investors. A more interesting question is what's in it for the bondholders? Under previous management, BlueLine's component businesses suffered operating losses in each of the prior three years. Then, too, according to the auditors, the process of integrating the dozens of acquisitions has revealed "material" weaknesses in the company's financial controls and information technology systems.

No doubt, Platinum Equity, with more than 150 acquisitions under its belt and 30 companies in its portfolio, means to fix the problems and return BlueLine to profitability. And if it succeeds, the creditors, too, would succeed, as success is modestly reckoned in the fixed-income world: They would get their money back, with interest.

As the BlueLine 93/4s are callable at 103 on Feb. 1, 2016, an investor's potential gains are hardly limitless. From today's price of 106.1, the securities would deliver a yield to call, or "worst," of 7.63%. To be sure, that would be a handsome gain for a fixed-income security. It would be less than overwhelming for an equity.

"The PIK toggle notes buyers are taking true equity risk, but their upside is capped," a paid-up subscriber who prefers to go unnamed tells colleague Evan Lorenz. "This is the inverse of a normal bondholder's position. You have all the downside risk, whether it is the economy slowing, rates moving higher, whether people start selling high yield because of the fear of all of the above." Looking back at the BlueLine 93/4s, our source suggests, the buyers will rue the day when they heard the words, "Sold to you."

"From what we see," our informant goes on, "it is probably the best time to be a long-short credit manager rather than just a long-only, buying new issues and hoping things go well." From the short seller's vantage point, the BlueLine PIK toggle notes have much to commend them. There are two problems, the coupon and--perhaps--the economy. Our source says that he does not intend to pull the trigger until business activity shows signs of decelerating.

On now to evidentiary sighting No. 2, which features our new best friend, Valeant Pharmaceuticals International (VRX on the Big Board). We won't repeat either our bearish analysis or our declaration of an interest (see the issue of Grant's dated March 7). Suffice it to say that Valeant is an acquisition machine, that the businesses it acquires tend not to prosper under Valeant management, that the Valeant front office is partial to non-GAAP measures of financial performance and that the company has generated positive GAAP net income in only three of the past eight quarters. Free cash flow in the fourth quarter amounted to $216 million, which, as Lorenz notes, "is actually less than the $241 million that Valeant generated in the second quarter of 2012--this despite a 152% jump in sales from the second quarter of '12 through the fourth quarter of '13."

A bear on Valeant might sell short the company's equity--or the opportunity to which we now turn, the company's single-B-rated, 63/8% senior unsecured notes of October 2020. There's much to be said for the latter approach.

Bulls and bears will go round and round on the nuances of purchase accounting as Valeant employs it, but there's no debating the debt; it ballooned to $16.9 billion at year-end 2013 from $6.5 billion at year-end 2011. Maybe Valeant's management can pull off the "merger of equals" it's been talking about. It would be a convenient way to de-lever the Valeant balance sheet. Or maybe Valeant's prospective merger partners will see the situation as we do. "While pharmaceutical executives have been happy to sell businesses and divisions to Valeant for cash," Lorenz points out, "my admittedly small sample of pharma contacts leads me to suspect that Valeant will have a hard time persuading a discerning appraiser of value to accept its stock. Then, too, creditors might begin to notice that Valeant's GAAP operating income in the fourth quarter failed to cover the company's $260.2 million in interest expense."

Whatever you may think of Valeant, the company, the Valeant 63/8s seem to offer only a modicum of upside. The notes change hands at 108.4 to yield 4.86%; that is the yield to maturity. The yield to the Oct. 15, 2016, call, a price of 103.19, works out to just 3.92%. As far as we can see, the creditor stands to be a loser--or, at least, not much of a winner--no matter how Valeant may fare in the next 21/2 years. Who would commit capital on these terms?

Why, the junk-bond funds would; they have to. The SPDR Barclays High Yield Bond ETF (JNK on the NYSE Arca) and the iShares iBoxx $ High Yield Corporate Bond ETF (HYG on the same exchange) count the Valeant note as their 17th and 21st largest holding, respectively. Junk funds need paper, especially the issues that weigh in at $2 billion-plus, as Valeant's does. Over the past four weeks, observes Martin Fridson, CEO of FridsonVision LLC (and a featured speaker at the April 8 Grant's Conference--advt.), net inflows into high-yield mutual funds enlarged the assets of those funds by 1.2% (this figure excludes inflows into the high-yield ETFs), whereas in February, the latest period for which data are available, the universe of non-investment-grade bonds expanded by only 0.3%. "The big picture," says Fridson, "is that there is not enough supply."

As every gold bull can attest, ETFs buy in bull markets and sell in bear markets. In the case of gold, a mitigating feature of the 37% price decline between Sept. 5, 2011, and Dec. 19, 2013, was the persistent purchase of physical bullion by Chinese and Indians. It's not so clear who would take the other side of a junk-bond liquidation.

Big, liquid issues--the ones that the ETFs like--"are the most vulnerable right now," Craig Kelleher, a partner in Boston-based Millstreet Capital Management, tells Lorenz. "We saw it in May last year. When those guys hit the 'sell' button, those large liquid names--they were perceived as liquid--can hit four- to five-point air pockets. ETFs now make up between 8% and 10% of the market and are predominantly in those large-cap names. Dealer inventories, as we know, are also at 10-year lows. Yet the high-yield market is multiples bigger than it was 10 years ago."

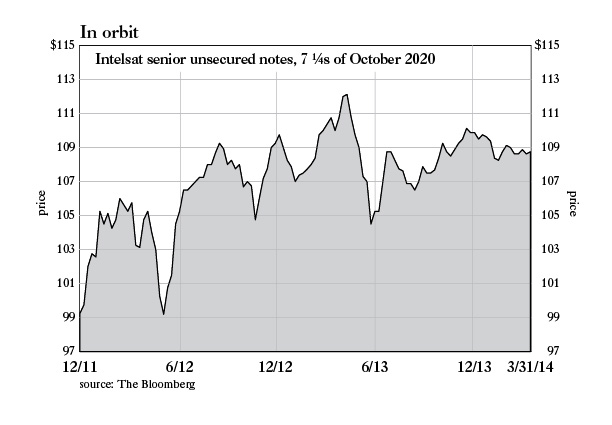

Intelsat senior unsecured notes, 7 ¼s of October 2020

Though America's economy, too, has grown over the past decade, it has lost that characteristic American oomph. Notably lacking in dynamism is, for instance, the regional gambling business. According to the Mississippi Gaming Commission, casino-generated tax revenue dropped by 4.7% in December from the like month a year earlier, to $18.2 million from $19.1 million. That is 37.5% less than the haul produced in December 2007 at the start of the Great Recession.

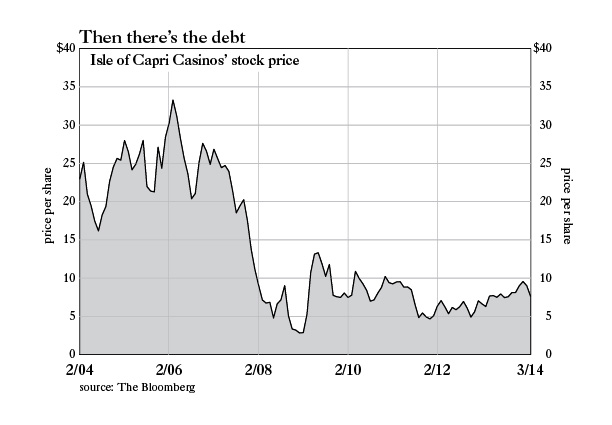

When casino licenses were hard to come by, therefore precious, public gambling businesses commanded fancy valuations, as our previously quoted anonymous source recalls. "Well," he says, "that is quickly eroding as more and more states, in a desperate grab for tax revenue, are willing to sell themselves to the devil and open up casinos." Isle of Capri Casinos (ISLE on the Nasdaq) is an example of an established gaming business that must regret the lawmakers' surrender to sin. Pricing of the company's single-B-rated 57/8s of March 2021--they trade at 102 to yield 5.52% to maturity--seems not to reflect that the house is facing more difficult odds.

Isle of Capri owns and operates 15 small casinos in Colorado, Florida, Iowa, Louisiana, Mississippi, Missouri and Pennsylvania; only four of them generate more than $20 million in annual operating profit. The average Isle of Capri customer, not a member of the 1%, doesn't have much to gamble with, let alone to lose.

And now comes more competition. A new Golden Nugget casino is slated to open late this year near the Lake Charles, La., property that accounted for $7.9 million in Isle of Capri operating profit over the past 12 months, or 12.5% of the grand total. According to a new report by Susan Berliner of J.P. Morgan, the Golden Nugget opening will likely skim 25% from Isle of Capri's take at Lake Charles.

(The rising young investor Bernard M. Baruch once talked himself out of an opportunity to do business with the elder J.P. Morgan by using the word "gamble" in the great man's presence; how times change.)

Then, too, Lorenz relates, more competition is on the way in Iowa, home to three of Isle of Capri properties, which together chipped in $37.6 million, or 60%, of the company's trailing 12 months' operating profit. Operating profit generated by Isle's profitable casinos sums to more than 100% of total operating profit owing to losses from casinos in Pennsylvania, Missouri and Mississippi. A March 2 story in the Quad-City Times made reference to plans for a new casino in Linn County, Iowa, a 47-mile drive from the Isle of Capri's Waterloo location. Even without new construction, the newspaper report said--here it cited a pair of independent research studies--"a saturated market is already under threat from Illinois' rapidly expanding video poker in taverns, stores and restaurants."

Our informant is short the Isle of Capri debt, despite the not remote chance of a change in corporate control. Some 40% of the outstanding shares are held by the family of the founder, Bernard Goldstein, who died in 2009. Assume, our source begins, that the family does sell, would you, the hypothetical buyer, be inclined to refinance a coupon as low as 57/8%? No, you would not, our source answers his own question, "especially if you are potentially adding more leverage to it." Besides, an observant buyer could hardly fail to notice that, in the fiscal quarter ended Jan. 26, Isle of Capri's $17.9 million in GAAP operating income failed to cover the company's $21.9 million in interest expense.

We close out this bears' beauty contest with an update on Intelsat SA (I on the NYSE). For the full chapter and verse, see the issue of Grant's dated Jan. 24. You may recall that the company operates 51 fixed satellites, a hugely expensive and time-consuming line of work (to launch one of these birds can cost up to $400 million and take from design to launch, three years). You may also remember that the satellite business requires growing revenue to leverage the high cost of operation. It doesn't help matters that various governments are building a dozen new satellites and contemplating the launch of several dozen more.

Fourth-quarter results, released on Feb. 20, featured operating income for 2013 in the sum of $1.2 billion, good enough to cover full-year interest expense by 1.08 times. For the year, revenue was $2.6 billion, a slight decrease from 2012. On the conference call, CEO and Chairman David McGlade said that, owing to reduced spending by the U.S. government and excess capacity in Africa, 2014 revenue is expected to total between $2.45 and $2.5 billion, a 4.9% year-over-year decline at the midpoint from 2013 results. Not to worry, the chief counseled dialers-in: "We remind our investors of our commitment to a two-phase investment model. The first several years of this plan is not dependent upon revenue growth but instead on the use of increasing cash flows to reduce our debt. We are sharply focused on de-levering to create equity value."

As of Dec. 31, there was $15.3 billion in total debt outstanding. On the call, the company announced plans to repay $400 million of that balance this year. Investors must bet that McGlade can do more with less revenue--in 2013, free cash flow amounted to $116.1 million and there is only $247.8 million of cash on the balance sheet.

To judge by the yields on Intelsat debt, bond investors have every confidence in McGlade--and in Janet Yellen, Jack Lew, Barack Obama and Vladimir Putin, besides. Thus, the single-B-plus-rated 71/4s of 2020 ($2.2 billion in par outstanding) change hands at 108.75, a yield to maturity of 5.63%. Inasmuch as the 71/4s are callable at 103.625 on October 2015, the yield that an optimistic holder may receive is likely to be closer to the yield to call, or "worst." That would be just 3.64%.

The best of times--the worst of times.

•

Not a subscriber? Click here