Gyro Gearloose redux .

Gyro Gearloose redux

Face-to-face with the Great Recession, central bankers hit the interest-rate-policy button; zero, as in "ZIRP," was the setting. Confronted with the punchless post-slump recovery, the Bank of Bernanke pulled the lever marked QE, for "quantitative easing." Today, presented with another case of the economic dwindles, the Bank of Yellen is said to be contemplating negative interest rates, as in "NIRP."

The arc of the evolution of monetary thinking is the subject in focus. What set us to writing was the realization that, with the talk about NIRP and a new plea from Bridgewater's Ray Dalio (of which more in a moment), monetary belief can be said to have nearly completed a 180-degree swing from the orthodoxy of yesteryear. We write to describe what happened and to speculate on what's in store. Skipping down to the bottom line, we address a question to the dollar-holding subscribers of Grant's: What's really in your wallet?

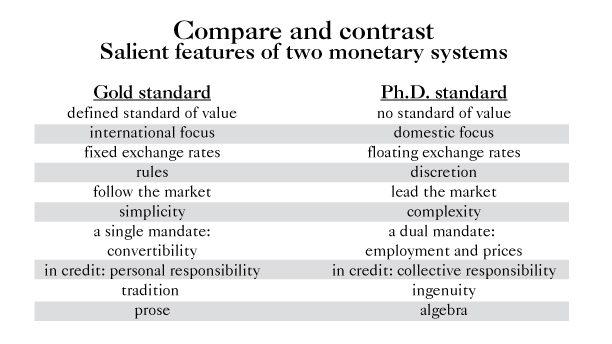

Salient features of two monetary systems

In doctrine, rigor and starch, the 21st-century Unitarian church bears no visible resemblance to the 17th-century Puritan church from which it is improbably descended. By the same token, the Ph.D. standard of monetary management shares no evident similarity with the gold standard--on the contrary, it's the antithesis of the gold standard. Still, the former is lineally descended from the latter. You can never predict how the kids will turn out.

Then, again, in the monetary family, perhaps you can. The long timeline of money begins with gold and silver. Next come credit instruments convertible into gold and silver. Then come credit instruments not quite convertible into gold and silver, though conceptually "backed" by the same. Finally--the year is now 1971--comes paper alone; pixels duly follow. Neither of these lightweight materials is a claim on "money," as previously defined. Each, rather, is ostensibly the thing itself. Governments have so ordered it, and we the people, for now, accept it. Contemplating this evolution, you could conclude that money wants to be easy and to become easier--less tangible, more profuse, less rule-bound. It's the same with credit, perhaps even more so.

Radical monetary policy begets still more radical monetary policy, which begets monetary tail risk. The experiments come thick and fast nowadays. Inhibitions are out the window. The central bankers talk matter-of-factly about "experiments" and "tool kits" and "models." They remind us of Gyro Gearloose, the oddball inventor in the old Disney comics. His inventions didn't always turn out the way he planned.

Last week, Dalio, founder of Bridgewater Associates, predicted a new phase of radical policy-making. Rather than infusing the banks' reserve accounts, the Fed would ultimately top up the people's bank accounts--just give away money, with the stipulation that the recipients spend it. "Helicopter money," the economists call this particular form of monetary destruction. Not that Dalio advocates such a thing, the billionaire hastened to add, only that he expects it. ZIRP is exhausted; QE, ditto. Investors and savers, he wrote, "will still want to save, lenders will still be cautious lenders and cautious borrowers will remain cautious, so we will still have 'pushing on a string.'?" What, exactly, the Fed may do of course remains to be seen. "Most importantly," Dalio closed, "central bankers need to put their thinking caps on."

U.K. bank rate*

Not take them off? Dalio has devoted his life to accumulating dollar bills. Of all people, you'd expect him to ask, "What is a dollar? What imbues it with value?" Yet he talks as cavalierly about monetary tinkering as do the Ph.D. tinkerers--he with his billions, they with their thousands.

On, now, to the work of casting today's monetary regime in the comparative light of its 19th-century forebear. The Gearloose inventions of the aftermath of 2008 have dulled the nervous sensors of the investment community, even those of the world's most successful hedge-fund manager. We mean to restore the feeling in those financial nerve endings.

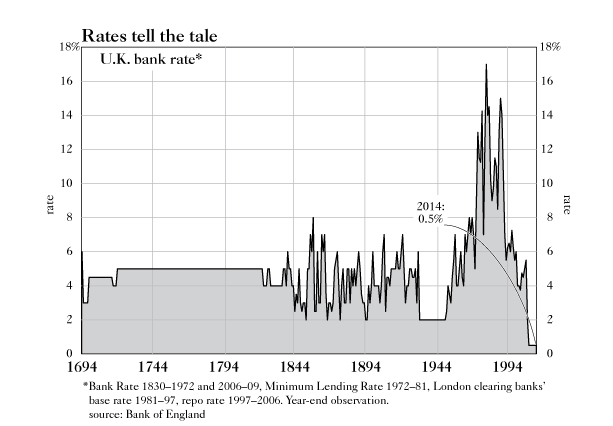

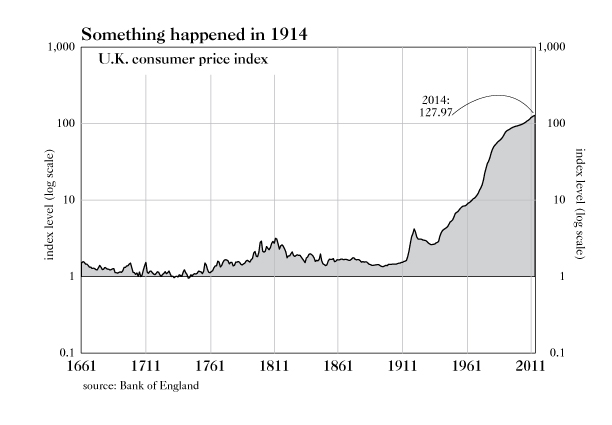

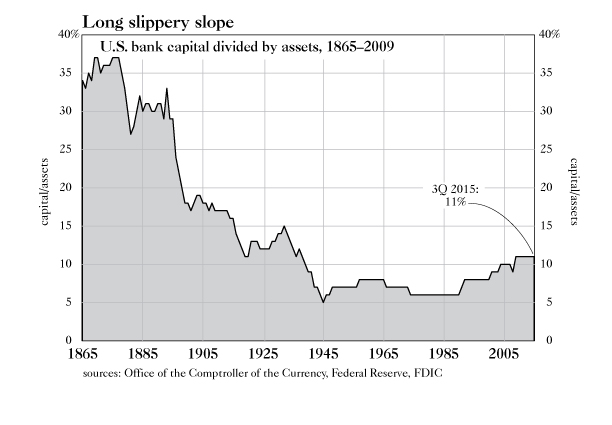

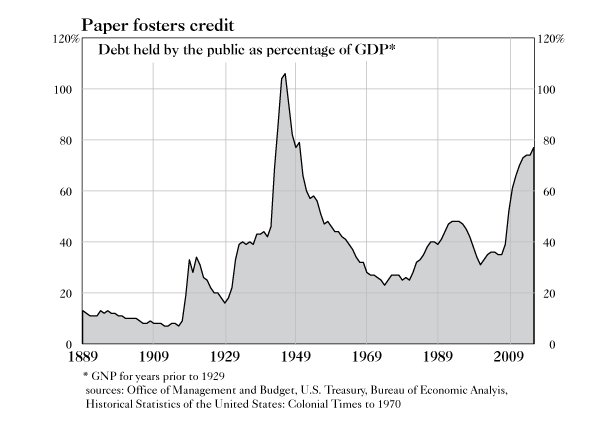

A glance at the table shows how far we have traveled, whether for good or ill is for you (and for Hillary and Ted, Bernie and Marco, Donald and Fox News) to decide. We ourselves submit into evidence the nearby graphs to illustrate the long-running decline in monetary order. Most illustrative, we judge, are those aberrant, post-World War II British interest rates, which touched highs and lows never before imagined. At a glance, an extraterrestrial visitor might conclude that the earthlings had left the gold standard.

In broad terms, the world has moved from rules to improvisation, from simplicity to complexity, from principles to "data dependency," from individual responsibility to collective responsibility, from a standard of value to no standard of value, from markets to mandarins, from tangibility in the monetary unit to abstraction in the monetary unit.

In times past, the standard of value was fixed while economic activity was left to fluctuate. Now, it's the trend growth in economic activity that--supposedly--is stable; monetary value is what gives way. It used to be said that the gold standard had a deflationary bias, the pure paper system an inflationary one. We deem this a slight mischaracterization. Gold had a bias to the stability of prices over the long run. Paper has a bias toward inflation over the long run. Equally, paper has a bias to credit formation, which is deflationary, over the medium and long run. Whether the final resolution of the world's desperate debts will take an inflationary or a deflationary course remains to be seen. Inflation remains our bet.

Under the economic tutelage of the great David Ricardo, Britain was the gold-standard nation par excellence. In the prosperous century between Waterloo and World War I, money was defined as a weight of metal, exchange rates were fixed, the stockholders of a bank were responsible for the solvency of the institution in which they owned a fractional interest, central bankers operated with only modest scope for discretionary action and the principal object of monetary policy was the convertibility of paper money into gold (and vice versa) at the statutory rate. The central bank took its policy cue not from employment or consumer prices but from the "state of exchanges." Such were the essentials of the classical gold standard.

U.K. consumer price index

These days, worldwide, money is undefined, exchange rates are floating or manipulated, the taxpayers (more so than the stockholders) are responsible for the solvency of the biggest banks, monetary policy is conducted with the widest scope for central-banking discretion and the principal object of that policy is domestic employment and price "stability" (meaning a targeted 2% rate of inflation). Such is the essence of the Ph.D. standard.

How did the latter system evolve from the former? Blame--or credit--the human animal, who wants stability and flexibility, rules and discretion, hard money and the counterfeit. One could say that the problem with money is credit and the problem with credit is people.

Plenty of thoughtful Victorians were unhappy with the monetary and credit arrangements of their day. They revered, most of them, the convertible pound. The fault they found was with the overextended banks and shadow banks (they had them, too).

Credit was the problem--credit is the problem. On this, our forebears and we can see eye-to-eye. The banker Samuel Jones Loyd, later Lord Overstone (1796–1883), one of the preeminent monetary thinkers of 19th-century Britain, contended that reckless credit would destroy a sound currency. In Britain, the problem lay with the bankers and bill brokers who funded themselves with interest-bearing demand deposits. The failure of one such aggressive depository institution could touch off a chain reaction of failures, as seemed to happen about once every 10 years. It was an "unsound and dangerous form of credit, [and] it cannot permanently coexist with an honest and well-regulated monetary system," Overstone said. "One or the other must succumb. If the credit system be too gigantic, and too powerful to be grappled with, we then only waste our time and labor in endeavoring to establish a sound monetary system."

U.S. bank capital divided by assets, 1865–2009

Overstone wrote those words as the Panic of 1857 howled. It was among the earliest of worldwide financial upheavals. Wholesale bankruptcies in America, the fast-growing overleveraged emerging market of the day, set the crisis in motion. Britain, the lordly creditor nation, succumbed in turn, because it, too, was overextended and America was its biggest trading partner. France and Germany were likewise tottering. The latter was laid low "from the inordinate extent of the paper currency, issued by all the states and even by the railway companies, and no specie [i.e., gold] to meet the demand for conversion," reported one of Overstone's scouts.

So credit, in one degree or another, had hijacked the gold standard. Especially was this so in America, where President James Buchanan, making his first address to Congress in December 1857, anticipated the wrath, if not the philosophy, of Sen. Elizabeth Warren (D., Mass.). Buchanan, a poor president but a penetrating monetary critic, lamented that so fabulously endowed a country as the United States had saddled itself with an "extravagant and vicious system of paper currency and bank credits, exciting the people to wild speculations and gambling in stocks. These [cyclical] revulsions must continue to recur at successive intervals so long as the amount of the paper currency and bank loans and discounts of the country shall be left to the discretion of 1,400 irresponsible banking institutions, which from the very law of their nature will consult the interest of their stockholders rather than the public welfare."

A bank must meet the demands of its depositors, the president went on. This meant paying out lawful money on the spot. Lawful money meant gold or silver.

The banks were in no condition to do anything of the kind. Collectively, they held less than one dollar of precious metals for every seven dollars in deposit and note liabilities (there was no national banking system, nor yet a national currency--the banks issued their own private label). Here was a remarkable fact, Buchanan paused to marvel. In 1848, before the California gold rush started, the banks had held very nearly one dollar of precious metals for every five dollars in deposit and note liabilities. Immense volumes of gold then found their way into the monetary system. Was this a gold inflation? Not on the evidence of the banking data. It was rather a credit inflation.

No Pangloss was Abraham Lincoln's immediate predecessor in the White House. He characterized the previous 40 years of American growth as a series of "extravagant expansions in the business of the country, followed by ruinous contractions. At successive intervals the best and most enterprising men have been tempted to their ruin by excessive bank loans of mere paper credit, exciting them to extravagant importations of foreign goods, wild speculations and ruinous and demoralizing stock gambling. When the crisis arrives, as arrive it must, the banks can extend no relief to the people. In a vain struggle to redeem their liabilities in [gold and silver] they are compelled to contract their loans and their issues, and at last, in the hour of distress, when their assistance is most needed, they and their debtors together sink into insolvency."

What was to be done? Buchanan urged Congress to pass a law that would "make it the irreversible organic law of each bank's existence that a suspension of [gold and silver] payments shall produce its civil death." Congress did no such thing (though a subsequent Congress, enacting Dodd-Frank, obligated big banks to plan for their civil death through so-called living wills).

The severe moralist is a stock figure in monetary history. Buchanan was one, Overstone was another. We, in our own way, play to the type. Reading the history of the 1857 smash, we have come to a new understanding of why and how the world has developed as it has. Or, at least, we recognize in the charges and counter-charges surrounding the events of 2008 and following, the echoes of long-ago grievances and crotchets.

The gold standard was evolved, not made. Gold, self-evidently a monetary metal--scarce, ductile, durable, easy on the eye--seemed ideally suited to the purpose. People preferred paper for ease of use, but paper was a claim, a derivative. The metal was, as the derivatives traders now say, the "underlying." Then, too, gold filled both a political and moral need. Without the limits imposed by gold convertibility, governments would surely abuse their monetary privilege.

Debt held by the public as percentage of GDP*

Before 1857, Britain might have seemed panic-proof. American banks were organized under the law of limited liability; the stockholders could lose only their investment plus the unpaid-in portion of their capital, if any; a failed bank would be no catastrophe for the average bank shareholder.

In Britain, liability was unlimited. The stockholders or partners were personally responsible for the debts of the bank in which they owned an equity interest. What better, or more certain, guardian of the integrity of a balance sheet than the focused attention of at-risk owners?

Of course, no human contrivance is people-proof. It happened that certain large English banks and, in particular, one very large English bill broker, were overextended, this sword of Damocles notwithstanding. Overend, Gurney & Company, familiarly known as Gurney's, was that broker. Destined to fail, or to "stop" (i.e., to stop paying gold) in 1866, the firm would live in 1857 thanks to emergency aid from the Bank of England. Shades of Goldman Sachs, Morgan Stanley and the rest of the modern supplicants, c. 2008.

England's central bank first met the crisis by boosting its discount rate to 10% in November from 5½% in October. You may wonder what it could possibly have been thinking about. It was thinking about its first remit, i.e., to protect the exchange rate. For this, it was necessary to attract gold to London and keep it there. Ten percent was a magnet.

The Bank of England, even then the lender of last resort, took another step, one more in keeping with 21st-century sensibility. It made common cause with the government to relax the Act of 1844, by which the Bank could extend credit only up to a certain fixed proportion of its gold reserve. It was the temporary suspension of that law, better known as Peel's Act, that saved the hide of English finance, many have contended.

George Arbuthnot, a well-placed British Treasury official, told Overstone that the Bank and the government had no choice but to give in. It was that or political and financial Armageddon. Yes, a stand on principle might have done good--would surely have done good in the long run. "But the immediate crisis would have been appalling," Arbuthnot argued, "and no British Ministry could have maintained itself in opposition to the cry which would have been raised."

Overstone was defiant. Perhaps his wealth--with an income of £100,000 a year and capital of £3–5 million, he was counted as one of his country's richest men--made no more difference to his monetary views than Dalio's wealth appears to make to his. Whatever the wellspring of his thought, Overstone harped on the cost of moral hazard. "The reckless speculators," the banker wrote to a friend as the discount rate reached 10%, "all who encourage or seek profit from the extravagant use of inflated credit, will proceed with more resolution than ever; knowing that a Government Letter [to suspend the 1844 act] is always in reserve for their assistance and protection; and that the certainty of its being issued depends, entirely upon the magnitude of their misdoings. If you overtrade moderately, and incur debts which you cannot pay, within a limited extent only, you will be left unassisted to find your own way out of difficulties of your own creation. But overtrade upon a gigantic scale and incur debts of a frightful magnitude--it then becomes an affair of public policy and you shall be assisted and protected for the public good."

Members of the English ruling class were properly grounded in the classical languages. Overstone closed his missive: "I now understand the meaning and force of Luther's dictum, Si peccas, pecca fortiter,"--which is to say, "If you sin, sin strongly."

Do you wonder what connects gold-standard orthodoxy with Ph.D.-standard heterodoxy? It is the human impulse to have it both ways--indeed, in this time of nonstop monetary intervention, seemingly all ways. As a financial species, we want hard money to save, easy money to spend and lots of credit to bridge the paydays. We would like to know the future, too: When will the Ph.D. standard blow up in the faces of the tinkerers?

We have no idea as to the timing of such a denouement but a clear view of the evolutionary arc. As to asset allocation: Duckburg, like New York City, had its own great mogul. He was Scrooge McDuck, a sometime patron of Gyro's workshop. Whatever else Scrooge might have owned, he owned gold.

•

Not a subscriber? Click here