Generation ZIRP

Online banks that are not quite banks walked the Wall Street red carpet last month. LendingClub (LC on the New York Stock Exchange), the world's biggest peer-to-peer lender, raised $1 billion in a Dec. 10 initial public offering. On Deck Capital (ONDK, also on the Big Board), a newfangled lender to small business, took in $230 million in a Dec. 16 IPO. Where these companies came from and where they're going are the subjects at hand. In preview, we judge each business to be susceptible to the time-honored risks of conventional lending as well as to the prospective risks of new forms of lending, adverse selection not least. Students of credit--not just the big, bad short-sellers--may profitably read on.

The credit cycle is eternal, this publication has come to believe. Lenders and borrowers may be reasonable people, but they periodically miscalculate. Under the spell of a central bank, they miscalculate together. First they overdo it, then they underdo it. There is feast, then there is famine, world without end.

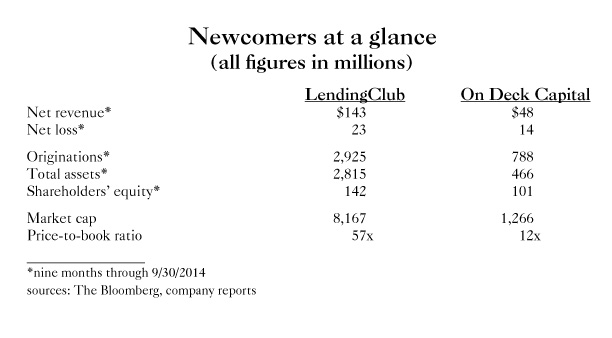

(all figures in millions)

It's the credit-related business models that come and go. An exception, to judge by the market's verdict, are the models under review here; to glance at the valuations, you'd suppose the respective companies have cured the credit cycle (as a page-one New York Times story on high-tech lending companies came close to doing on Monday), or possibly pattern baldness. On Deck changes hands at 12 times book value, LendingClub at 57 times book value.

The LendingClub stratagem is half Uber, half eHarmony. Strip away cost, substitute algorithms for bank branches and loan officers, and match debtors with creditors. "Better rates. Together," is the motto. On Deck does more than broker credit formation; it borrows in the wholesale market and lends in the retail market, putting its own credit at risk. At LendingClub, in contrast, credit risk resides not on the balance sheet but with the lenders. Each company is fast growing. Neither is profitable.

Both are children of post-crisis finance. The Federal Reserve has blessed them with ground-hugging interest rates and punitive regulation--punitive, that is, to the ordinary banks with which the newcomers compete. Technology, too, smiles on the fledglings, though just how well today's automated lending protocols will function in a future recession remains to be seen.

Even without net income, LendingClub commands a market cap in excess of $8 billion, a size that could win it admission to the S&P 500 (constituent companies D.R. Horton and H&R Block aren't worth much more). It's no small achievement for a business that, as recently as 2011, booked revenue of just $12.8 million. Growth is what the market's paying for, that and the conviction that LendingClub has truly built a better mousetrap. "We operate at 400 to 500 basis points lower than the banks and have customer satisfaction rates that are multiple times greater than the banks," founder and CEO Renaud Laplanche tells Forbes's Steven Bertoni. "If you look at the history of tech-driven innovations, there aren't a lot of examples where the incumbents could compete with an innovator--look at Amazon vs. Borders or Netflix vs. Blockbuster."

Or look, say we, at the Chicago Mercantile Exchange back in the year 2000, when it was supposedly about to be run out of business by the likes of EMerge Interactive (EMRG), an online cattle brokerage and auction service, then valued at 50 times book value and commanding a $2 billion market cap. Only one of the two is still around, and it isn't EMerge, which filed for bankruptcy protection in 2007 (see Grant's, March 17, 2000).

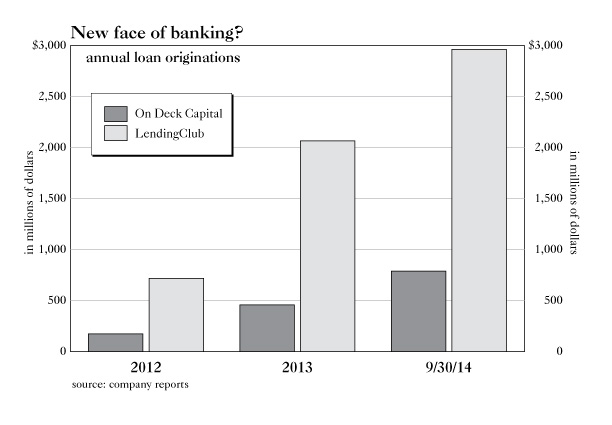

Be that as it may, in the nine months through Sept. 30, LendingClub's top line reached $143 million. In the third quarter of 2014, the company facilitated $1.2 billion of lending and borrowing. It was a large and telling portion of the grand total of $6.2 billion of transactions that LC has brokered since its 2006 inception ("We are doubling originations each year," says Laplanche). Mary Meeker, John Mack and Larry Summers are among the stars who stud the LendingClub board; they joined in 2012. Google owns an 8% LendingClub stake; it invested in 2013.

Let us say that you are sick and tired of paying 17% on a credit-card balance or--a slightly more problematical situation--you can't get a mortgage but you would like a house. You log into LendingClub, disclose your income and FICO score and how much you want to borrow ($14,182 is the average), and for what purpose (debt consolidation is the No. 1 stated use of proceeds). The bull story on Lending Club makes much of the fact that the typical borrower shows a 699 FICO score (near the average for American consumers) and declares $73,000 of personal income (in the top 10% of personal income). This is no post-crisis reenactment of the subprime mortgage debacle, insists Mark Palmer, analyst at BTIG Research. Lending Club--or for that matter, Prosper, its top closely held competitor--are more than conscientious screeners of credit, "particularly with regard to FICO scores, but also all the other variables they're using in their credit models," says Palmer. "It's over 100 factors."

annual loan originations

Or let us say you are sick and tired of earning zero at the bank. You, too--in the capacity of a lender--log in. At LendingClub, you stand to earn a great deal more than zero. On average, at last report, borrowers paid rates ranging between 12.07% for three years to 16.92% for five years; this is the gross. What lenders earn after fees and credit losses is substantially less. Since inception, it has averaged between 4.74% and 8.32%. Lenders can pick and choose options on the LendingClub credit menu to diversity across the quality and maturity spectrum. They receive monthly checks as interest and principal are paid. Of course, some borrowers don't pay on time and some don't pay at all. "LendingClub notes are not insured or guaranteed and investors may have negative returns," says the fine print.

Anyway, the posted average historical returns are handsome rates of pay in a yield famine. "At the lower-yielding end," relates colleague Charley Grant, "one would have to stretch to earn the equivalent in the liquid capital markets. Triple-B-rated Colombia would do the trick if you didn't mind a little duration risk. The dollar-denominated Colombia 5.625s of 2044 trade at 112 to yield 4.85%. At the higher-yielding end, you could match the historical LendingClub return with a 28-year investment in Caa1/B-rated Greece; the Greek 2s of 2042 change hands in the low 50s to yield 8.2%. Given how slim are the pickings, it's hardly surprising that yield-starved institutions are flocking to the peer-to-peer portal: 'While LendingClub's business was once focused purely on consumer loan deals struck between individuals,' the Financial Times reported last week, 'more than half of its loans are now said to be funded by large professional investors such as hedge funds and wealth managers.'"

LendingClub and On Deck are different businesses with distinct similarities. Business lending, not consumer lending, is On Deck's stock in trade, and On Deck funds itself in the wholesale market rather than in the retail market. Those differences are starting to blur. Last week brought news that LC, in collaboration with Google (which, incidentally, also happens to own a small stake in On Deck), will try to make a splash in business credit.

Common to both neophyte lenders are the margin-fattening consequences of ultra-low interest rates. In the case of On Deck, 53.2% is the average annualized rate it charged its evidently desperate clientele in the third quarter, down from 65.9% in the first quarter of 2013. The cost of its liabilities, meanwhile, has fallen to 6.6% in the nine months through Sept. 30, 2014, from 13.4% in calendar 2012.

You'd suppose that a business willing to borrow at On Deck's rates would fail to tick every standard prudential box. Charge-offs peaked at 9% of loans outstanding in 2008; 6.2% were written off in 2013. Incomplete results in 2014 indicate a drop in the charge-off rate to 1.5%. For perspective, according to the Federal Reserve, charge-offs of commercial and industrial loans at regulated banks peaked at 2.66% in the fourth quarter of 2009. At last report--the third quarter of 2014--they registered at 0.2%. Then, again, vig on the order of 50% was unavailable to the average commercial banker.

"For LendingClub," Grant finds, "net cumulative lifetime charge-off rates on 36-month loans tracked by annual vintage show a general trend of improving credit quality--perhaps not a surprise since the data series begins in 2008. For 36-month term loans originated in 2008, charge-offs reached 14.7% by month 36. For 2009 and 2010 originations, that figure falls to 9% and 6.2% at the 36th month mark. For loans booked in 2011-14, there are partial data only. Through 35 months, 5.2% of 2011 loans have been written off; this compares favorably to prior years (6.1% was the rate at month 35 for 2010 originations). Loans booked in 2012 are not so strong through 25 months; 5.9% is the latest charge-off reading, which is higher than at comparable points in 2010 (5.3%) and 2011 (4.3%). For 2013, we have 14 months of data, for which the charge-off rate is 1.9%, the strongest on record (2.1% was the comparable figure in 2011). So far, so good in 2014: through four months, charge-offs stand at 0%.

As for Brand X--the regulated banks--credit-card charge-offs peaked at 11% in the second quarter of 2010. At last report, which is the third quarter of 2014, they had dwindled to 2.89%," Grant continues. "Let it be noted that these two ratios do not lend themselves to a direct comparison. Unlike LendingClub and On Deck, which calculate charge-offs as a percentage of annual originations, the Fed measures charge-offs as a percentage of total loans."

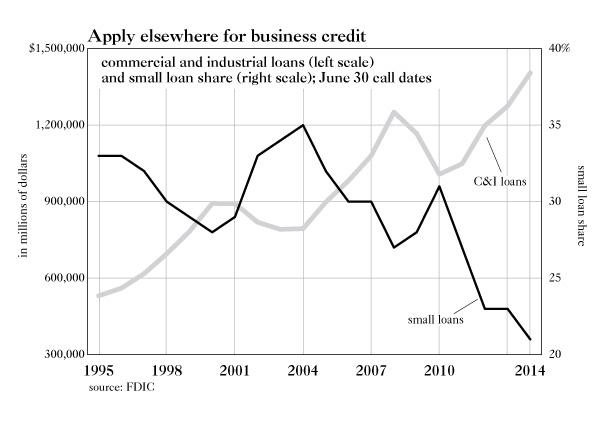

commercial and industrial loans (left scale) and small loan share (right scale); June 30 call dates

Of course, interest-rate suppression was only one government response to the financial crisis. Asphyxiating regulation was another. For all intents and purposes, contends Richard Bove, analyst with Rafferty Capital Markets, the banking industry has been nationalized. "By that I mean," Bove tells Grant, "basically the government tells the banks what the size of their assets should be. If they go above those sizes, the government hits them with capital penalties. Then the government says, OK, we're going to tell you how to allocate your assets between loans and other areas. And then the government goes into liquid assets and says, 'Well, these are high-quality liquid assets and these are not,' so you have to go to the high-quality area, and it [the government] goes into your loan portfolio and it tells these banks, 'This is where we're going to allow you to have low-risk weightings and therefore we want to lend there, and this is where you can't lend."

Bove went on: "Then it goes to the liabilities side of the balance sheet and it says, 'Look, we don't want you to do short-term borrowing, because if you do short-term borrowing, then basically you're creating a systemic risk in the repo market. We want you to do long-term borrowing. 'Then they put a few hundred people in the big banks and they make the big banks pay for those people, even though those people work for the government. The job of those people is to make sure the bank does what the government says. Now you've created this huge vacuum, right? And this vacuum is, people want or need money that banks are not allowed to give them, and therefore you create the opportunity for a LendingClub or an On Deck Capital, and those companies pursued it very aggressively, very successfully."

Business lending--and small-business lending, especially--has dwindled in the wake of the crisis. Thus, commercial and industrial loans from regulated banks to American borrowers have inched ahead by just 1.94% a year over the past six years. For context, C&I loan growth compounded at 7.3% per annum from 2002 to 2008. And business loans of less than $1 million, as a percentage of overall business loans, stand at just 21% today, the lowest figure in the 20 years for which the FDIC keeps data (35% of C&I loans fell under the $1 million mark in 2004).

"Just ask the bankers, as the Federal Reserve Bank did in September in conjunction with the Conference of State Bank Supervisors," Grant reports. "A questionnaire asked bankers which of 20 enumerated services they planned to offer in the next three years. A significant plurality of the 1,008 respondents, roughly 40%, replied 'none of the above.' Possibly some of the refuse-niks were thinking about the FDIC's post-crisis actions to hold directors of failed banks personally responsible for the loans that sank their institutions. David Baris, a partner at BuckleySandler LLP and president of the American Association of Bank Directors, tells me that worries about personal liability do more than merely scare off qualified candidates for bank boards: 'Undoubtedly,' Baris says, 'fear of personal liability has had a big impact on the kinds of loans that are approved, given the risk that directors are willing to take in approving loans. Our advice has been for bank directors not to approve loans at all. All these things have a chilling effect on credit availability, on the willingness of qualified persons to serve as directors, and if they do serve, on how they serve.'"

At last report, $859 billion in revolving consumer credit and $298 billion in small business loans were outstanding. Prosper, the closely held peer-to-peer portal, has facilitated $2 billion in credit. LendingClub, as noted, has brokered $6.2 billion and On Deck has placed $1.7 billion. For the bulls' money, the opportunity to profit by the federal fatwa on conventional banking (and on the ostensibly obsolete economics of conventional lending) remains wide open.

Of course, LendingClub and its ilk may themselves wind up in the regulatory net. The risk section of the LendingClub prospectus warns that the Consumer Financial Protection Bureau, the regulatory brainchild of Sen. Elizabeth Warren (D., Mass.), could make mischief. Then, too, the banking industry, however dispirited it might be, hasn't fired its lobbyists. "Several lawsuits," to quote the prospectus, "have sought to re-characterize certain loan marketers and other originators as lenders. If litigation on similar theories were successful against us, loans facilitated through our platform could be subject to state consumer protection laws in a greater number of states."

Credit and funding may prove more substantive risks than regulation. As to credit, there's nothing very new about algorithmic lending methods. They were state of the art in 2005-07, too, as FICO scores, algorithms and third-party techniques based on digital inputs began to displace the people who had previously picked up the phone to verify employment, salary and the rest. "Now," says Bove, "in good times, that works. In bad times, it doesn't. What happens to these companies in bad times is that they lose access to funding. Banks don't lose access to funding because they get FDIC insurance."

Wholesale funding, as a rule, is fair weather funding. It vanished for Continental Illinois way back in 1984, and for Northern Rock and Bear Stearns in the not so distant past of the global financial crisis. "We depend on debt facilities and other forms of debt in order to finance most of the loans we make to our customers," On Deck acknowledges in its IPO filing. "However, we cannot guarantee that these financing sources will continue to be available beyond the current maturity date of each debt facility, on reasonable terms or at all."

The asset side of the On Deck balance sheet, too, is risk fraught, the prospectus notes. Maybe, for instance, the company's maiden securitization of business loans in May 2014 (i.e., the refashioning of individual credits into a marketable security) won't be the start of something big and sustainable after all. "If we were unable to arrange new or alternative methods of financing on favorable terms," as the legal language puts it, "we may have to curtail our origination of loans, which could have a material adverse effect on our business, financial condition, operating results and cash flow."

"All of which," Grant observes, "raises the question of just how different On Deck really is from the ordinary business-focused commercial bank--apart from the fact that it takes no deposits, that it holds equity capital equivalent to 5% of assets (as against 9.5% for the average FDIC-insured bank), that it charges interest rates that make you do a double take and that it's valued at 12 times book, double the price-to-book ratio of any American-domiciled bank known to Bloomberg. Then, too, On Deck's net interest margins--22.1% so far in 2014--are outsize."

What is the life expectancy of a business that borrows at 50% or 60% during an economic expansion? What kind of consumer pays 14% in a time of miniature mortgage rates? "Anyone who is not able to establish reasonable credit is going to stay with On Deck and LendingClub and borrow more and more money," Bove says. "So the net-net of it is, ultimately, these companies will make a fortune in the next couple of years and then, because of negative selectivity, they're going to fight a terrible battle to stay alive."

Final word goes to a successful commercial lender who operates in a different market segment with a different M.O. "I am bearish on the brilliance of predictive lending models with such limited data," says our authority, who asks to go nameless. "I am bullish on the capabilities of fraudsters to exploit them, and I am bullish on the intelligence of most business owners."

Note to the bears: To borrow On Deck shares will cost you 7 ¼%, LendingClub, 1.25%. As to timing of a short sale, it would be very nice to wait until the cusp of the next recession. When might that be? We are working on the relevant algo.

•

Not a subscriber? Click here